Financial Accounting Solved Question Papers November' 2015Dibrugarh University B.Com 1st Sem2015 (November) - Semester

(NEW COURSE)

Full Marks: 80

Pass Marks: 24

1. (a) Fill in the blanks: 1x4=4

- Balance Sheet is also known as Position Statement.

- In hire-purchase system, the buyer charges depreciation on Cash price.

- Royalty Account is closed by transferring to Production or Profit and Loss Account.

- Branches are generally classified into Three types.

(b) Write ‘True’ or ‘False’: 1x4=4

- Profit & Loss Account shows the financial position of a concern. False, Operating efficiency

- Profit on repossession of goods sold on hire-purchase system is a capital profit.

- Shortworkings is the excess of minimum rent over actual royalty.

- In Departmental Accounts, each department is considered as a separate profit centre.

2. Write short notes on (any four): 4x4=16

Ans: Accounting Standards are the policy documents or written statements issued, from time to time, by an apex expert accounting body in relation to various aspects of measurement, treatment and disclosure of accounting transactions for ensuring uniformity in accounting practices and reporting. These standards are prepared by Accounting Standard Board (ASB). Accounting Standards are formulated with a view to harmonies different accounting policies and practices in use in a country. It was established in the year 1977.

- Termination of hire-purchase agreement.

Ans: Ans: The hire-purchase agreement stipulates the circumstances in which the agreement can be terminated. The agreement is generally terminated by return of the goods by the hirer, notice of termination by the owner on account of hirers breach of conditions or notice of termination by the hirer. The hirer may, at Dairy time before the final payment under the hire-purchase agreement falls due, and after giving the owner not less than fourteen days’ notice in writing of his intention so to do, terminate the hire-purchase agreement. Where a hire-purchase agreement is terminated under this Act, then the owner shall be entitled to retain the hire which has already been paid and to recover the arrears of’ hire due.

- Goods-in-transit.

Ans: Goods in transit: When goods are dispatched by the head office to branch and the branch does not receive it even upto the end of the year, it is known as goods in transit. In the same way when goods are returned by branch to head office and the head office does not receive it upto the end of the year it is also known as goods in transit.

It is quite understandable that a difference should arise in the balances of two accounts due to these transactions. Therefore, to reconcile, the following journal entry will be passed in head office books in both the circumstances:

Goods in Transit a/c Dr.

To Branch a/c

(Goods in transit taken into books)

In the Balance Sheet of Head office both the above items will be shown as an asset.

- Principles of allocation of common expenses among departments.

Ans: Allocation of Expenses

Departmental Expenses: The expenses of a business can be broadly divided into following two categories:

1. Direct expenses: Expense relating to a particular department are called direct expenses. They are charged to respective department. For example wages, staff salaries, material etc.

2. Indirect Expenses: Expenses relating to more than one department are called indirect expenses. They are further divided into:

(a) Expenses which can be allocated

(b) Expenses which cannot be allocated

Allocation and Apportionment of Departmental Expenses

(1) There are certain expenses which can be specially incurred for a particular department. Such expenses are charged directly to the department.

(2) There are certain expenses which are indirect in nature and incurred for the whole department. Such expenses are distributed amongst various departments on some suitable basis. The following table will help to know the proper basis for apportionment of some important expenses among various departments.

Expenses

|

Basis

|

|

|

(3) There are certain expenses which cannot be allocated on some equitable basis such as debenture interest, dividend, share transfer fees, general office expenses, income tax etc. and thus should not be apportioned. Profits of all departments should be brought down in one total and such expenses should be debited and non-departmental profits credited to this without making any effort for its apportionment amount different departments in Combined income account.

- Shortworkings.

Ans: Shortworkings

The excess of minimum rent over royalty is called ‘Shortworkings’. It is calculated with the help of following formula: Minimum Rent – Royalty = Shortworkings. Normally, Shortworkings arises during gestation period or due to abnormal working conditions or during the early periods of lease as the activity level is low in that period.

Shortworkings should be carried forward and shown on the assets side in the Balance Sheet so long as they are recoverable and Shortworkings which could not be recouped during the allowed period of recoupment should be closed by transferring to profit and loss account. If there is no provision in the royalty agreement for recoupment of Shortworkings, the same should be transferred to profit and loss account in the year of the Shortworkings. The questions of Shortworkings or its recoupment does not arises if the royalty agreement does not contain a clause of minimum rent.

3. (a) What do you mean by ‘Accounting Standards’? Mention the procedure for issuing Accounting Standards. Distinguish between Accounting Standards and Accounting Principles. 2+6+6=14

Ans: ACCOUNTING STANDARDS

Accounting Standards are the policy documents or written statements issued, from time to time, by an apex expert accounting body in relation to various aspects of measurement, treatment and disclosure of accounting transactions for ensuring uniformity in accounting practices and reporting. These standards are prepared by Accounting Standard Board (ASB). Accounting Standards are formulated with a view to harmonies different accounting policies and practices in use in a country.

Procedure adopted in formulation of Accounting Standards:

The Institute of Chartered Accountants of India (ICAI), recognising the need to harmonies the diverse accounting policies and practices, constituted an Accounting Standards Board (ASB) on April 21, 1977. The main function of ASB is to formulate accounting standards so that such standards may be mandated by the Council of ICAI. While formulating the standards in India, ASB will take into consideration the applicable laws, customs, usages and business environment.

Following procedure will be adopted for formulating Accounting Standards:

- Identification of the broad areas by the ASB for formulating the Accounting Standards.

- Constitution of the study groups by the ASB for preparing the preliminary drafts of the proposed Accounting Standards.

- Consideration of the preliminary draft prepared by the study group by the ASB and revision, if any, of the draft on the basis of deliberations at the ASB.

- Circulation of the draft, so revised, among the Council members of the ICAI and 12 specified outside bodies such as Standing Conference of Public Enterprises (SCOPE), Indian Banks’ Association, Confederation of Indian Industry (CII), Securities and Exchange Board of India (SEBI), Comptroller and Auditor General of India (C& AG), and Department of Company Affairs, for comments.

- Meeting with the representatives of specified outside bodies to ascertain their views on the draft of the proposed Accounting Standard.

- Finalisation of the Exposure Draft of the proposed Accounting Standard on the basis of comments received and discussion with the representatives of specified outside bodies.

- Issuance of the Exposure Draft inviting public comments.

- Consideration of the comments received on the Exposure Draft and finalisation of the draft Accounting Standard by the ASB for submission to the Council of the ICAI for its consideration and approval for issuance.

- Consideration of the draft Accounting Standard by the Council of the Institute, and if found necessary, modification of the draft in consultation with the ASB.

- The Accounting Standard, so finalised, is issued under the authority of the Council.

Or

(b) The following is the Trial Balance of Ajay and Bijay, a partnership firm as on 31st March, 2015:

Trial Balance

Debit Balances

|

Rs.

|

Credit Balances

|

Rs.

|

Opening Stock

Machinery

Purchases (adjusted)

Salary

Wages

Buildings

Insurance

Freight

Conveyance

Carriage Inwards

House Rent

Returns Inward

Carriage Outwards

Sundry Debtors

Bills Receivable

Cash in Hand

Drawings:

Ajay

Bijay

Closing Stock

|

24,500

50,000

1,30,000

10,000

14,000

60,000

500

3,000

1,400

3,850

2,400

1,600

2,400

18,000

5,250

2,300

3,600

4,200

38,000

|

General Reserve

Reserve for Doubtful Debts

Sales

Sundry Creditors

Ajay’s Loan (Taken on 01.10.2014)

Bills Payable

Bad Debts Recovered

Capital:

Ajay

Bijay

|

38,000

500

2,35,000

33,700

8,000

9,350

450

30,000

20,000

|

3,75,000

|

3,75,000

|

Prepare a Trading and Profit & Loss Account for the year ended 31st March, 2015 and Balance Sheet as on that date taking into consideration the following information: 4+5+5=14

- On 29.02.2015, a fire broke out in the godown and goods worth Rs. 7,000 were destroyed, goods being insured, the insurance company admitted a claim for Rs. 6,000.

- Reserve for Doubtful Debts is to be maintained at 5% of Sundry Debtors.

Solution:

Trading and Profit & Loss A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Opening Stock

To Purchases 1,30,000

Less: Loss by fire 7,000

To Wages

To Freight

To Carriage Inwards

To Gross Profit c/d

|

24,500

1,23,000

14,000

3,000

3,850

65,050

|

By Sales 2,35,000

Less: Returns 1,600

|

2,33,400

|

2,34,000

|

2,34,000

| ||

To Loss by fire

To Salary

To Insurance

To Conveyance

To Carriage Outwards

To Reserve for D/D

To Interest on Ajay Loan

To Net Profit

- Ajay = 49,560/2 = 36,130

- Bijay = 49,560/2 = 36,130

|

1,000

10,000

500

1,400

2,400

900

240

49,560

|

By Gross Profit b/d

By Provision for d/d

By Bad debts recovered

|

65,050

500

450

|

66,000

|

66,000

|

Partner’s Capital A/c

Particulars

|

Ajay

|

Bijay

|

Particulars

|

Ajay

|

Bijay

|

To Drawings

To House Rent

To Balance c/d

|

3,600

1,200

49,980

|

4,200

1,200

39,380

|

By Balance b/d

By Share of Profit

|

30,000

24,780

|

20,000

24,780

|

54,780

|

44,780

|

54,780

|

44,780

|

Balance Sheet

Liabilities

|

Amount

|

Assets

|

Amount

|

General Reserve

Sundry Creditors

Ajay’s Loan 8,000

Add: Interest on

Ajay’s Loan @ 6% 240

Bills Payable

Capital:

Ajay 49,980

Bijay 39,380

|

38,000

33,700

8,240

9,350

89,360

|

Insurance Claim

Machinery

Buildings

Sundry Debtors 18,000

Less: Reserve for d/d 900

Bills Receivable

Cash in hand

Closing Stock

|

6,000

50,000

60,000

17,100

5,250

2,300

38,000

|

1,78,650

|

1,78,650

|

4. (a) What is ‘hire-purchase system’? What are its important features? Distinguish between hire-purchase system and instalment-purchase system. 3+5+6=14

Ans: Hire Purchase - Meaning: A trader could sell goods either for cash or for credit. For goods sold on credit, the payments may be made by the buyer in lump sum on a future date, or in installments spread over for a specified period of time. When goods are sold on credit, for which payment is made by the buyer in installments over a period of time, it is called purchase system or installment system.

Hire Purchase System defers to the system wherein, the seller of goods transfer the goods to the buyer without transferring the ownership of goods. The payment for the goods will be made by the buyer in installments. If the buyer pays all the installments, the ownership of the goods will be transferred, on payment of the last installment. However, if the buyer does not pay for any installment, the goods will be repossessed by the seller and the money paid on earlier installments will be treated as hire charges for using the goods. So, under this system, the transaction may result in purchasing of goods by the buyer or in hiring the goods. Hence, the system is called Hire Purchase System.

Characteristics of Hire-Purchase System

The characteristics of hire-purchase system are as under

- Hire-purchase is a system of credit sale.

- The price under hire-purchase system is paid in installments.

- The goods are delivered in the possession of the purchaser at the time of commencement of the agreement.

- Hire vendor continues to be the owner of the goods till the payment of last installment.

- The hire-purchaser has a right to use the goods as a bailer.

- The hire-purchaser has a right to terminate the agreement at any time in the capacity of a hirer.

- The hire-purchaser becomes the owner of the goods after the payment of all installments as per the agreement.

- If there is a default in the payment of any installment, the hire vendor will take away the goods from the possession of the purchaser without refunding him any amount.

Differences Between Hire Purchase System and Installment Purchase System:

Hire-Purchase System

|

Installment Purchase

|

It is a contract of hiring.

|

It is a contract of sale.

|

It is transferred by seller to buyer only after payment of all installments.

|

It is transferred by seller to buyer, immediately on signing the contract.

|

In this case, the buyer is like a bailee

|

In this case, the buyer is not in the position of a bailee

|

Such risk is on the seller.

|

Such risk is on the buyer.

|

On default of payment of any installment by the buyer, the seller can repossess the goods.

|

On default and payment of any installment by the buyer, seller cannot repossess the goods, but can file a suit in the court of law against the buyer for the recovery of unpaid price.

|

The buyer can exercise the option of return of goods.

|

The buyer cannot exercise the option of return of goods.

|

The buyer cannot dispose the goods, until the payment of last installment. If disposed, the third party buyer does not get a better title.

|

The buyer has the right to dispose the goods, even if all installments are not yet paid.

|

Or

(b) Nikhil purchased a machine on hire-purchase system for Rs. 1,12,000. Down payment is to be made Rs. 30,000 and the remaining part is to be paid in three instalments of Rs. 30,000 each at the end of each year. Rate of interest is charged at 5% per annum and Nikhil is depreciating the machine at 10% per annum on written-down value method. Because of financial difficulties, Nikhil after having paid down payment of Rs. 30,000 and first instalment at the end of first year, could not pay second instalment and the seller took possession of the machine. Seller after spending Rs. 1,700 on repairs, sold it away for Rs. 62,000. Show the Ledger Accounts in the books of Nikhil and the seller to record the transactions. 4+4+4+2=14

Solution:

Calculation of Interest:

Rs.

| |

Cash Price (1st Year)

Less: Down Payment

|

1,12,000

30,000

|

Add: Interest @ 5%

|

82,000

4,100

|

Less: 1st Installment

|

86,100

30,000

|

2nd Year

Add: Interest @ 5%

|

56,100

2,805

|

Repossession value

|

58,905

|

Calculation of Depreciation:

Rs.

| |

Cash Price

Less: Depreciation @ 10%

|

1,12,000

11,200

|

B.V (2nd Year)

Less: Repossession value

|

1,00,800

58,905

|

Loss of Repossession

|

41,895

|

Calculation of Profit & Loss If the Vendor/Seller:

Rs.

| |

Repossession Value

Add: Expenses

|

58,905

1,700

|

Less: Sale of Machinery

|

60,605

62,000

|

Profit

|

1,395

|

LEDGER

In the books of Vendee (Nikhil)

Machinery A/c

Dr. Cr.

Date

|

Particulars

|

Amount

|

Date

|

Particulars

|

Amount

|

1st Year

|

To Vendor A/c

|

1,12,000

|

1st Year

|

By Depreciation A/c

By Balance c/d

|

11,200

1,00,800

|

1,12,000

|

1,12,000

| ||||

2nd Year

|

To Balance b/d

|

1,00,800

|

2nd Year

|

By Vendor A/c

By Profit & Loss A/c

|

58,905

41,895

|

1,00,800

|

1,00,800

|

Vendor A/c

Dr. Cr.

Date

|

Particulars

|

Amount

|

Date

|

Particulars

|

Amount

|

1st Year

|

To Bank A/c

To Bank A/c

To Balance c/d

|

30,000

30,000

56,100

|

1st Year

|

By Machinery A/c

By Interest A/c

|

1,12,000

4,100

|

1,16,100

|

1,16,100

| ||||

2nd Year

|

To Machinery A/c

|

58,905

|

2nd Year

|

By Balance b/d

By Interest

|

56,100

2,805

|

58,905

|

58,905

|

LEDGER

In the books of Vendor

(Nikhil) A/c

Dr. Cr.

Date

|

Particulars

|

Amount

|

Date

|

Particulars

|

Amount

|

1st Year

|

To H.P. Sales A/c

To Interest A/c

|

1,12,000

4,100

|

1st Year

|

By Bank A/c

By Bank A/c

By Balance c/d

|

30,000

30,000

56,100

|

1,16,100

|

1,16,100

| ||||

2nd Year

|

To Balance b/d

To Interest A/c

|

56,100

2,805

|

2nd Year

|

By Goods repossessed

|

58,905

|

58,905

|

58,905

|

Goods Repossessed A/c

Dr. Cr.

Date

|

Particulars

|

Amount

|

Date

|

Particulars

|

Amount

|

2nd

Year

|

To Nikhil A/c

To Bank A/c (DD)

To Profit & Loss A/c (Profit of vendor)

|

58,905

1,700

1,395

|

2nd Year

|

By Bank A/c (Sold)

|

62,000

|

62,000

|

62,000

|

5. (a) (i) What do you mean by ‘branch’ and ‘department’? 2+2=4

Ans: Branch: A branch is a separate segment of a business. In order to increase the sales, business houses are requires to market their products over a larger territory and may generally split their business into certain divisions or parts. These various parts or divisions may be located in different part of the same city or in different cities of the same country or in different countries in the world. These are known as branches. The head office controls the activities of various branches.

Department: Department refers to activity centre (profit or cost centre) usually located in the same roof but carrying distinct type of activities.

(ii) Distinguish between Branch Accounts and Departmental Accounts. 5

Ans: Distinction between Departmental Accounts and Branch Accounts

The main distinctions between Departmental Accounts and Branch Accounts are given below:

Basis of Distinction

|

Departmental Accounts

|

Branch Accounts

|

Maintenance of Accounts

|

All accounts are maintained at one place & departmental trading and profit and loss account is prepared accordingly.

|

In case of branch, all branch accounts are kept at Head Office except cash, customers and stock registers are maintained at branch. But in case of independent branch all accounts are kept at branch and a branch prepares its own trading and Profit & Loss Account.

|

Allocation of Common Expenses

|

Departments are not geographically separated from each other, so problem of allocation of common expenses among different departments arises.

|

As branches are geographically separated from each other so the problem of allocation of common expenses among different branches does not arises.

|

Adjustments & Reconciliation of Accounts

|

The question of adjustments and reconciliation of accounts does not arise in departmental accounts.

|

In case of independent branch some adjustments and reconciliation of head office and the branch accounts are required to be done at the end of the year.

|

Problem of foreign currency

|

The problem of conversion of foreign currency into home currency does not arise.

|

The problem of conversion of foreign branch figures may arise at the time of finalization of accounts of head office.

|

Reason for creation

|

Departments are the result of fast human life.

|

Branches are the outcome of tough competition and expansion of business.

|

Functional Division of accounts

|

Functional division is possible in case of departmental trading which is a must for the existence of a department.

|

It is not possible in case of a branch trading.

|

Segmentation and Condensation

|

Departmental Accounting is practically a segment of accounts.

|

Branch Accounting is a condensation of accounts.

|

(iii) How are the inter-departmental transactions recorded in Departmental Accounts? 5

Ans: Inter departmental transfers

Transfer of goods or services by one department to another department are called inter departmental transfers. When one department transfers goods to another department, the transaction should be considered as a sale for the supplying department and a purchase for the receiving department. As such, the supplying department should be credited and the receiving department should be debited with the value of goods supplied.

Similarly, when one department renders service to another department, the department rendering the service should be credited and the department receiving the service should be debited with the value of service rendered.

Goods may be transferred either at cost price or at selling price. If goods are transferred at selling price by the transferor department and such goods are unsold at the end of the accounting year by the transferee department, then profit charged on such unsold goods by the transferor department is treated as unrealized profit and it should be debited to the general profit and loss account as stock reserve. In the balance sheet stock reserve should be deducted from closing stock. If unrealized profit is contained in the opening stock, such reserve should be credited to the general profit and loss account.

Calculation and Treatment of Unrealized Profit

To calculate Stock Reserve, the following steps must be followed:

Step 1: Calculate the value of IDT (inter Department transfer) by using the following formula:

Closing Stock of Transferor dept x IDT / Total Direct expenses excluding op stock

Step 2: The value of step 1 denotes the Value of IDT stock included in Transferee dept. Now calculate the GP (Gross Profit) ratio at which transferor dept sells goods to transferee. i.e. this amount is at selling price. GP ratio is to be calculated on SP to eliminate Unrealized Profit i.e. St. reserve with the help of following formula:

GP ratio on sales = (GP of Transferor Dept / Total sales) /100

Where Total sales = Normal sales + IDT sales

Step 3: Result of Step 1 x Result of Step 2

Treatment: The following journal entry is to be passed to eliminate the amount of unrealized profit:

General P & L A/c

To Stock Reserve A/c

Note: In next year the stock reserve of current year will become realised and to be credited to P & L a/c

Or

(b) The Lakhimpur Head Office supplies goods to its branch at Jorhat at cost. The branch sells the goods for cash and on credit and remits the proceeds to the Head Office promptly. The branch expenses being met by the head Office by cheque. The following are the transactions relating to the branch for the year ended 31st March, 2015:

Stock at branch on 01.04.2014

Debtors at branch on 01.04.2014

Goods sent to branch during the year

Total sales at branch (including cash sales Rs. 2,20,000)

Goods returned by branch

Goods returned by customers

Collection from debtors

Discount allowed

Bad debts written off

|

Rs.

60,000

80,000

4,50,000

7,40,000

20,000

20,000

4,20,000

20,000

10,000

|

Cheque sent by Head Office towards the branch expenses:

Salaries

Rent

Petty expenses

Stock at branch on 31.03.2015

|

Rs.

50,000

25,000

5,000

90,000

|

Prepare Branch Account and goods sent to Branch Account in the books of Head Office. Also, prepare Branch Debtors Account in a working note. 8+4+2=14

Dibrugarh Branch A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Opening balance

Stock

Debtors

To Goods sent to branch 4,50,000

Less: Return by branch (20,000)

To Bank Exp.

Salaries

Rent

Petty Exp.

To General P/L A/c

|

60,000

80,000

4,30,000

50,000

25,000

5,000

2,10,000

|

By Remittance

Cash sales

Collection from Debtors

By Closing balance

Stock

Debtors

|

2,20,000

4,20,000

90,000

1,30,000

|

8,60,000

|

8,60,000

|

Goods Sent to Branch A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Dibrugarh Branch A/c (Return)

To Balance c/d

|

20,000

4,30,000

|

By Dibrugarh Branch A/c

|

4,50,000

|

4,50,000

|

4,50,000

|

Branch Debtors A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Opening balance

To Credit sales

|

80,000

5,20,000

|

By Cash (Remittance)

By Goods return by customer

By Discount allowed

By Bad debt

By Closing balance

|

4,20,000

20,000

20,000

10,000

1,30,000

|

6,00,000

|

6,00,000

|

6. (a) (i) What is ‘minimum rent’ in Royalty Account? Why is it important in Royalty Account? 3+3=6

Ans: Minimum Rent is the amount below which landlord never accepts in any year from the person who has to pay royalty in case of mines. Minimum Rent is also known as Fixed Rent, Dead Rent, Flat Rent or Contract Rent. If in any year amount of royalty is less than the amount of minimum rent, the amount of minimum rent is payable by the person who has to pay the royalty, but if the amount of royalty is more than the amount of minimum rent, royalty will be paid.

Importance of Minimum Rent:

Fixation of minimum rent is in the interest of landlord because it guarantees him the receipt of the minimum rent even in the case of low output or sales. In the absence of minimum rent clause, only the actual royalty will be paid to the landlord. Moreover, it also gives incentive to the lessee to enhance production or sales because he is bound to pay minimum rent.

(ii) What conditions are to be satisfied for recoupment of Shortworkings? 4

Ans: Conditions for Recoupment or Writing off Shortworkings: Shortworkings can be recouped only when there is surplus. The Recoupment may be permitted over a stipulated period of time (fixed Recoupment) or over a specified period following the year of short working (floating Recoupment) or within the life time of the lease(Recoupment within life time of the lease). All the conditions regarding recoupment or writing off Shortworkings are based on the mutual agreement between the lessee and lessor. If Shortworkings could not be recouped within the agreed period, it will be transferred to profit and loss account in the year in which the right of recoupment is lost. By this process, Shortworkings account gets closed and will not appear as an asset in the balance sheet.

(iii) Distinguish between ‘Rent’ and ‘Royalty’. 4

Ans: Difference between Royalties and Rent:

In the common usage, the term royalty is used to mean rent. But there is some difference between royalty and rent. The following are the major difference between royalty and rent:

S.N.

|

Royalty

|

Rent

|

|

Royalty is the consideration payable for the use of special right for both tangible and intangible assets.

|

But rent is the consideration payable for the use of only tangible assets.

|

|

Royalty is paid either on the basis of output or sale.

|

Rent is paid on the basis of period.

|

|

Royalty varies on the basis of output or sales.

|

Rent is fixed.

|

|

Royalty agreement normally contains a clause to pay a minimum rent.

|

But in rent, there is no concept of minimum rent.

|

|

Parties are known as lessor and lessee.

|

Parties are known as tenant and landlord.

|

Or

(b) Mohan Deka took a colliery from Jatin Chaudhury on lease for a period of 15 years from 1st January, 2008, on a royalty of Rs. 16 per ton of coal raised with a minimum rent of Rs. 80,000 per annum and power to recoup short-workings during the first four years of the lease. The annual coals raised were:

Year 2008

Year 2009

Year 2010

Year 2011

Year 2012

|

3000 tons

3500 tons

5000 tons

9000 tons

10000 tons

|

From the above particulars, prepare (i) Royalty Account, (ii) Jatin Chaudhury’s Account and (iii) Short-workings Account in the books of Mohan Deka. 5+5+4=14

Solution:

ANALYSIS OF ROYALTIES PAYABLE:

Year

|

Output

|

Royalty

@ Rs. 16

|

M/R

|

Shortworking

|

Surplus

|

Recoupment

|

Written off

|

Payment

|

2008-09

2009-10

2010-11

2011-12

2012-13

|

3,000

3,500

5,000

9,000

10,000

|

48,000

56,000

80,000

1,44,000

1,60,000

|

80,000

80,000

80,000

80,000

80,000

|

32,000

24,000

-

-

-

|

-

-

-

64,000

80,000

|

-

-

-

56,000

-

|

-

-

-

-

-

|

80,000

80,000

80,000

88,000

1,60,000

|

Royalties A/c

In the books of Sri Mohan Deka (Lessee)

Date

|

Particulars

|

Amount (Dr.)

|

Date

|

Particulars

|

Amount (Cr.)

|

31-3-09

|

To Jatin Chaudhury

|

48,000

|

31-3-09

|

By Production A/c

|

48,000

|

48,000

|

48,000

| ||||

31-3-10

|

To Jatin Chaudhury

|

56,000

|

31-3-10

|

By Production A/c

|

56,000

|

56,000

|

56,000

| ||||

31-3-11

|

To Jatin Chaudhury

|

80,000

|

31-3-11

|

By Production A/c

|

80,000

|

80,000

|

80,000

| ||||

31-3-12

31-3-12

|

To Jatin Chaudhury

To Shortworking A/c

|

88,000

56,000

|

31-3-12

|

By Production A/c

|

1,44,000

|

1,44,000

|

1,44,000

| ||||

31-3-13

|

To Jatin Chaudhury

|

1,60,000

|

31-3-13

|

By Production A/c

|

1,60,000

|

1,60,000

|

1,60,000

|

Jatin Chaudhury A/c

Date

|

Particulars

|

Amount (Dr.)

|

Date

|

Particulars

|

Amount (Cr.)

|

31-3-09

|

To Bank A/c

|

80,000

|

31-3-09

31-3-09

|

By Royalties A/c

By Shortworking A/c

|

48,000

32,000

|

80,000

|

80,000

| ||||

31-3-10

|

To Bank A/c

|

80,000

|

31-3-10

31-3-10

|

By Royalties A/c

By Shortworking A/c

|

56,000

24,000

|

80,000

|

80,000

| ||||

31-3-11

|

To Bank A/c

|

80,000

|

31-3-11

|

By Royalties A/c

|

80,000

|

80,000

|

80,000

| ||||

31-3-12

|

To Bank A/c

|

88,000

|

31-3-12

|

By Royalties A/c

(1,44,000 – 56,000)

|

88,000

|

88,000

|

88,000

| ||||

31-3-13

|

To Bank A/c

|

1,60,000

|

31-3-13

|

By Royalties A/c

|

1,60,000

|

1,60,000

|

1,60,000

|

Dr. Shortworking A/c Cr.

Date

|

Particulars

|

Amount (Dr.)

|

Date

|

Particulars

|

Amount (Cr.)

|

31-3-09

|

To Jatin Chaudhury A/c

|

32,000

|

31-3-09

|

By Balance c/d

|

32,000

|

32,000

|

32,000

| ||||

1-4-09

31-3-10

|

To Balance b/d

Ti Jatin Chaudhury A/c

|

32,000

24,000

|

31-3-10

|

By Balance c/d

|

56,000

|

56,000

|

56,000

| ||||

1-4-10

|

To Balance b/d

|

56,000

|

31-3-11

|

By Balance c/d

|

56,000

|

56,000

|

56,000

| ||||

1-4-11

|

To Balance b/d

|

56,000

|

31-3-12

|

By Royalties A/c

|

56,000

|

56,000

|

56,000

|

(OLD COURSE)

Full Marks: 80

Pass Marks: 32

Time: 3 hours

1. (a) Write ‘Correct’ or ‘Incorrect’ : 1x4=4

- Unearned Income Account is a liability. True

- Cost of goods sold on hire-purchase is transferred to hire-purchase Trading Account. True

- Minimum Rent is also known as ‘Rock Rent’ in Royalty Account. True

- When a partner is not able to meet his liabilities, he is said to be solvent. True

(b) Fill in the blanks: 1x4=4

- Valuation of inventories is accounted for as per the Accounting Standard 2.

- Hire-purchase transactions are controlled by the Hire-Purchase Act of 1972.

- Royalty paid on sales is debited to Profit and Loss Account.

- If inventory at branch is shown at invoice price instead of cost price, then the account which is used for adjustment is Stock reserve Account.

2. Write short notes on (any four): 4x4=16

- International Financial Reporting Standards (IFRS).

Ans: International Financial Reporting Standards (IFRS)

IFRS is a set of international accounting standards stating how particular types of transactions and other events should be reported in financial statements. IFRS are generally principles-based standards and seek to avoid a rule-book mentality. Application of IFRS requires exercise of judgment by the preparer and the auditor in applying principles of accounting on the basis of the economic substance of transactions. IFRS are issued by the International Accounting Standards Board (IASB). IASB issued only thirteen (13) IFRS which are as follows:

IFRS 1 - First-time adoption of International Financial Reporting Standards

IFRS 2 - Share-based payment

IFRS 3 - Business combinations

IFRS 4 - Insurance contracts

IFRS 5 - Non-current assets held for sale and discontinued operations

IFRS 6 - Exploration for and evaluation of mineral resources

IFRS 7 - Financial instruments: disclosures

IFRS 8 - Operating segments

IFRS 9 - Financial instruments

IFRS 10 - Consolidated financial statements

IFRS 11- Joint arrangements

IFRS 12- Disclosure of interests in other entities

IFRS 13- Fair Value measurement

Need and Importance of IFRS

The goal of IFRS is to provide a global framework for how public companies prepare and disclose their financial statements. IFRS provides general guidance for the preparation of financial statements, rather than setting rules for industry-specific reporting. Having an international standard is especially important for large companies that have subsidiaries in different countries. Adopting a single set of world-wide standards will simplify accounting procedures by allowing a company to use one reporting language throughout. A single standard will also provide investors and auditors with a comprehensive view of finances.

- Instalment Purchase System.

Ans: INSTALMENT PURCHASE SYSTEM

Meaning: Installment payment system (also called the deferred installments) is a system where the buyer is given the ownership as well as the possession of the gods at the time of signing the contract. The buyer has the facility to pay the price in installments.

Definition: According to J.B. Batliboi, Installment Purchase System is a system under there is an agreement to purchase and pay by installments, the goods which become the property of the Purchaser immediately when he receives the delivery of the same.

Features of Installment Payment System:

The features of Installment payment are as follows:

- Under this system, there will be an outright sale of goods/assets.

- The possession as well as the ownership is passed to the buyer right at the time of signing the contract.

- The buyer can make the payment in installments.

- IN case of default in payment, the seller cannot repossess the goods, but he can sue the buyer for the recovery of unpaid price.

- The buyer cannot exercise the option of returning the goods and terminate the contract, unless the same becomes void or voidable under the contract act.

- Goods-in-transit.

Ans: Goods in transit: When goods are dispatched by the head office to branch and the branch does not receive it even upto the end of the year, it is known as goods in transit. In the same way when goods are returned by branch to head office and the head office does not receive it upto the end of the year it is also known as goods in transit.

It is quite understandable that a difference should arise in the balances of two accounts due to these transactions. Therefore, to reconcile, the following journal entry will be passed in head office books in both the circumstances:

Goods in Transit a/c Dr.

To Branch a/c

(Goods in transit taken into books)

In the Balance Sheet of Head office both the above items will be shown as an asset.

- Lease.

- Rules of Garner vs. Murray.

3. (a) (i) What do you mean by the basic concepts and conventions of accounting? 2+2=4

Ans: Accounting Conventions: Certain accounting conventions are followed while preparing financial statements such as convention of ‘Conservatism’, convention of ‘Materiality’, convention of ‘Full disclosure’, convention of ‘Consistency’. According to convention of ‘Conservatism’, provisions are made of expected losses but expected profits are ignored. This means that the real financial position of the business may be better than what has been shown by the financial statements. The use of accounting conventions makes financial statements simple, comparable, and realistic.

Accounting Concepts: While preparing financial statements the accountants make a number of assumptions known as accounting concepts such as going concern concept, money measurement concept, realisation concept, etc. According to the going concern concept, it is assumed that the business of the concern shall be continued indefinitely. The assets are shown in the balance sheet at their book value rather than their market value.

(ii) Write a note on Accounting Standard Board set up in India. 4

Ans: Accounting Standards are the policy documents or written statements issued, from time to time, by an apex expert accounting body in relation to various aspects of measurement, treatment and disclosure of accounting transactions for ensuring uniformity in accounting practices and reporting. These standards are prepared by Accounting Standard Board (ASB). Accounting Standards are formulated with a view to harmonies different accounting policies and practices in use in a country. It was established in the year 1977.

(iii) Distinguish between Accounting Standards and Accounting Principles. 4

Ans: Difference between Accounting Standard and Accounting Principles

Accounting Standard is the set of rules that should be applied for measurement, valuation, presentation and disclosure of a subject matter. For example, measurement of deferred tax, valuation of assets, intangibles and financial instruments etc. and presentation and disclosure of such measurements and valuations.

Accounting Principles however, are the fundamental principles providing a framework within which accounting should be done. These principles also govern the formulation of Accounting Standards. For example, Accrual accounting, Substance over legal form, Prudence etc.

Or

(b) Akash and Bikash are partners of a partnership business. The Trial Balance of their firm as on 31st March, 2015 was as under:

Trial Balance

Debit Balances

|

Rs.

|

Credit Balances

|

Rs.

|

Land and Buildings

Machinery

Drawings:

Akash

Bikash

Salaries and Wages

Furniture

Trade Expenses

Sundry Debtors

Discount

Insurance

Advertising

Cash at Bank

Bills Receivable

Closing stock (on 31.03.2015)

|

40,000

18,000

2,000

3,500

3,700

6,500

1,900

24,600

1,000

1,200

3,000

2,900

4,000

36,000

|

Trading Account (Gross Profit)

Capital:

Akash

Bikash

Provision for Doubtful Debts

General Reserve

Sundry Creditors

Outstanding Wages

Bank Loan

(on 01.10.2014)

|

60,000

35,000

25,000

800

4,000

15,000

500

8,000

|

1,48,300

|

1,48,300

|

Prepare a Profit & Loss Account and a Profit & Loss Appropriation Account for the year ended 31st March, 2015 and a Balance Sheet as on that date considering the following adjustments: 5+2+5=12

- Write off bad debts Rs. 600 and provided for doubtful debts @ 5% on remaining debtors.

- Provide for interest on capital @ 5% per annum.

- Provide for interest on bank loan @ 10% per annum.

- Provide depreciation @ 10% p.a. on land and Buildings, @ 12 ½% p.a. on machinery and @ 5% p.a. on furniture.

- Write off ¼ of advertising.

Solution:

Profit & Loss A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Depreciation on Land & Buildings

To Depreciation on Machinery

To Salaries and Wages

To Depreciation on Furniture

To Trade Expenses

To Bad debts

To Provision for d/d

To Discount

To Insurance

To Advertising

To Interest on Bank Loan

To Net Profit

|

4,000

2,250

3,700

325

1,900

600

1,200

1,000

1,200

750

400

43,475

|

By Gross Profit b/d

By Provision for D/d

|

60,000

800

|

60,800

|

60,800

|

Profit & Loss Appropriation A/c

(Dr) (Cr)

Particulars

|

Amount

|

Particulars

|

Amount

|

To Interest on Capital:

Akash = 35,000 x 5%

Bikash = 25,000 x 5%

To Share of Profit:

Akash = 40,475 x 1/2

Bikash = 40,475 x ½

|

1,750

1,250

20,237.5

20,237.5

|

By Net Profit b/d

|

43,475

|

43,475

|

43,475

|

Partner’s Capital A/c

Particulars

|

Akash

|

Bikash

|

Particulars

|

Akash

|

Bikash

|

To Drawings

To Balance c/d

|

2,000

54,987.5

|

3,500

42,987.50

|

By Balance b/d

By Interest on Capital

By P/L Appropriation A/c

|

35,000

1,750

20,237.5

|

25,000

1,250

20,237.5

|

56,987.5

|

46,487.50

|

56,987.5

|

46,487.50

|

Balance Sheet

Liabilities

|

Amount

|

Assets

|

Amount

|

General Reserve

Sundry Creditors

Outstanding Wages

Bank Loan 8,000

Add: Interest on Bank Loan 400

Capital Accounts:

Akash = 54,987.50

Bikash = 42,987.50

|

4,000

15,000

500

8,400

97,975

|

Land & Building 40,000

Less: Depreciation @ 10% 4,000

Machinery 18,000

Less: Depreciation @ 12.5% 2,250

Furniture 6,500

Less: Depreciation @ 5% 325

Sundry Debtors 24,600

Less: Bad debts 600

24,000

Less: Provision for d/d 5% 1,200

Advertisement

Cash at Bank

Bills Receivable

Closing Stock

|

36,000

15,750

6,175

22,800

2,250

2,900

4,000

36,000

|

1,25,875

|

1,25,875

|

4. (a) Distinguish between credit sale and sale under hire-purchase system. Mention any three rights of hire seller and three rights of hire purchaser as laid down in the Hire-Purchase Act, 1972. 5+3+3=11

Ans: Differences Between Hire Purchase System and Installment Purchase System:

Hire-Purchase System

|

Installment Purchase

|

It is a contract of hiring.

|

It is a contract of sale.

|

It is transferred by seller to buyer only after payment of all installments.

|

It is transferred by seller to buyer, immediately on signing the contract.

|

In this case, the buyer is like a bailee

|

In this case, the buyer is not in the position of a bailee

|

Such risk is on the seller.

|

Such risk is on the buyer.

|

On default of payment of any installment by the buyer, the seller can repossess the goods.

|

On default and payment of any installment by the buyer, seller cannot repossess the goods, but can file a suit in the court of law against the buyer for the recovery of unpaid price.

|

The buyer can exercise the option of return of goods.

|

The buyer cannot exercise the option of return of goods.

|

The buyer cannot dispose the goods, until the payment of last installment. If disposed, the third party buyer does not get a better title.

|

The buyer has the right to dispose the goods, even if all installments are not yet paid.

|

Rights and Obligations of the Hirer and Owner

RIGHTS OF THE HIRER

- Right of hirer to purchase at any time with rebate: The hirer may, at may time during the continuance of the hire-purchase agreement and after giving the owner not less than fourteen days notice in writing of his intention so to do, complete the purchase of the goods by paying or tendering to the owner the hire-purchase price or the balance thereof as reduced by the rebate.

- Right of hirer to terminate agreement at any time: The hirer may, at Dairy time before the final payment under the hire-purchase agreement falls due, and after giving the owner not less than fourteen days’ notice in writing of his intention so to do, terminate the hire-purchase agreement.

- Right to appropriate payments in respect of two or more agreements in such proportions as he thinks fit.

- Assignment and transmission of hirer’s rights or interest under hire-purchase agreement: The hirer may assign his right, title and interest under the hire-purchase agreement with the consent of the owner, or, if his consent is unreasonably withheld, without his consent.

- Rights of hirer in case of seizure of goods by owner: Where the owner seizes the goods let under a hire-purchase agreement, the hirer may recover from the owner the amount, if any, by which the hire-purchase price falls short of the aggregate of the following amounts, namely the date

- The amounts paid in respect of the hire-purchase price up to the date of seizure;

- The value of the goods on the date of seizure.

RIGHTS OF THE OWNER

- Rights of owner to terminate hire-purchase agreement for default in payment of hire or authorised act or breach of express conditions: Where a hirer makes more than one default in the payment of hire-purchase agreement then, subject to the provisions of Section 21 and after giving the hirer notice in writing of not less than-

- One week, in a case where the hire is payable at weekly or lesser intervals; and

- Two weeks, in any other case,

The owner shall be entitled to terminate the agreement by giving the hirer notice of termination in writing:

- Rights of owner on termination: Where a hire-purchase agreement is terminated under this Act, then the owner shall be entitled to retain the hire which has already been paid and to recover the arrears of’ hire due.

Or

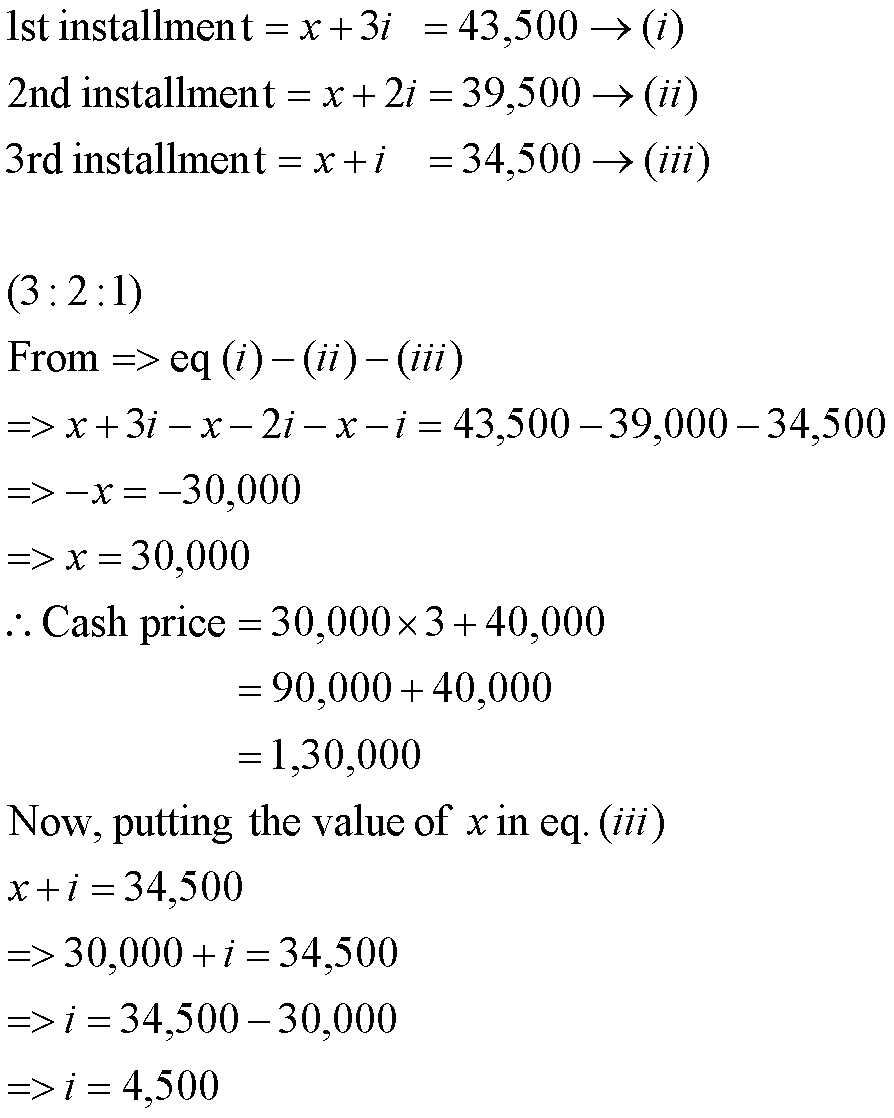

(b) Kumarendra purchased a motor cycle on hire-purchase system from M/s Bora & Co. The terms of hire-purchase are:

Down payment

1st instalment

2nd instalment

3rd instalment

|

Rs.

40,000

43,500

39,000

34,500

|

All instalments are payment at the end of the year and each instalment includes equal amount of cash price in addition to interest. Prepare necessary Ledger Accounts in the books of the Buyer. 11

Solution:

When Cash Price and rate of interest is missing:

Installment = Part of cash price + Interest

Let, The part of cash price including each installment = X, Interest = Y

Now,

Ledger

In the books of Manabendra & Company

M/S Sarma & Co.

Dr. Cr.

Date

|

Particulars

|

Amount

|

Date

|

Particulars

|

Amount

|

1st Year

|

To Bank A/c

To Bank A/c

To Balance c/d

|

40,000

43,500

60,000

|

1st Year

|

By Machinery A/c

By Interest A/c

|

1,30,000

13,500

|

1,43,500

|

1,43,500

| ||||

2nd Year

|

To Bank A/c

To Balance c/d

|

39,000

30,000

|

2nd Year

|

By Balance b/d

By Interest A/c

|

60,000

9,000

|

69,000

|

69,000

| ||||

3rd year

|

To Bank A/c

|

34,500

|

3rd year

|

By Balance b/d

By Interest A/c

|

30,000

4,500

|

34,500

|

34,500

|

5. (a) (i) What do you mean by inter-branch transactions? Mention about the different methods of recording such transactions. 2+4=6

Ans: Inter-Branch Transactions: Where there are number of branches, inter-branch transactions are likely to take place, e.g., cash or goods sent by one branch to another or expenses incurred by one branch on behalf of another. Such transactions are usually adjusted assuming that they were entered into under the instructions from the H.O. Suppose Kolkata branch transfers some goods to Mumbai branch under the directions of the H.O. The entries will be as follows:

1.

|

In the books of Kolkata Branch:

Head Office A/c Dr

To Goods Supplied to Branch A/c

|

XXX

|

XXX

|

2.

|

In the books of Mumbai Branch:

Goods received from Branches A/c Dr

To Head Office A/c

|

XXX

|

XXX

|

3.

|

In the books of Head Office:

Mumbai Branch A/c Dr

To Kolkata Branch a/c

|

XXX

|

XXX

|

Note: Inter-branch transactions without the knowledge of head office may be passed as between the branches only in the usual manner.

(ii) Discuss about the main objectives of Branch Accounts. 5

Ans: Objectives of Branch Accounting: The following are the main objects of maintaining branch accounts:

- Profit or loss of each branch can be found out

- They help in controlling branches

- Actual financial position of the business can be found out on the basis of head office and branch accounting periods.

- Branch requirements of goods and cash can be estimated.

- Suggestions for increasing the efficiency of the branch can be sent on the basis of branch accounts.

- They help in complying with the requirements of law because acc to companies act 2013.

Or

(b) Jorhat Head Office sent out goods to its Golaghat Branch at cost plus 25%. The branch remits all cash received to the Head Office and all expenses of the branch are met by the Head Office. From the following particular, prepare (i) Golaghat Branch Account and (ii) Branch Debtors Account in the books of the Head Office. 5+3+3=11

Stock at branch on 01.04.2014 (Invoice price)

Stock at branch on 31.03.2015 (Invoice price)

Goods sent to branch during the year (Invoice price)

Goods returned by the branch (Invoice price)

Cash Sales

Credit Sales

Goods returned by customers

Discount and allowance to customers

Bad Debts

Cash received from customers

Sundry Debtors as on 01.04.2014

|

Rs.

17,500

18,750

13,75,000

75,000

3,00,000

9,98,750

40,000

60,000

5,000

10,45,000

2,40,000

|

Cheques sent to branch:

For Salaries

For Rent

For Sundry expenses

|

Rs.

1,00,000

24,000

25,000

|

Solution:

In the books of Head office

Golaghat Branch A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Opening balance

Stock to branch

Debtors to branch

To Goods sent to branch 13,75,000

Less: Return by branch (75,000)

To Bank Exp.

Salaries

Rent

Sundry Exp.

To Stock Reserve on (Closing)

(

To General P/L A/c

|

17,500

2,40,000

13,00,000

1,00,000

24,000

25,000

3,750

5,750

|

By Remittance

Cash sales

Collection from Debtors

By Stock Reserve on (Opening)

(

By Goods sent to branch

(

By Closing balance

Stock at branch

Debtors at branch

|

3,00,000

10,45,000

3,500

2,60,000

18,750

88,750

|

17,16,000

|

17,16,000

|

Branch Debtors A/c

Particulars

|

Amount

|

Particulars

|

Amount

|

To Opening balance

To Credit sales

|

2,40,000

9,98,750

|

By Cash (Remittance)

By Goods return by customer

By Discount allowed

By Bad debt

By Closing balance

|

10,45,000

40,000

60,000

5,000

88,750

|

12,38,750

|

12,38,750

|

6. (a) (i) What is ‘minimum rent’ in Royalty Account? Why is it important in Royalty Account? 3+3=6

Ans: Minimum Rent: Minimum Rent is the amount below which landlord never accepts in any year from the person who has to pay royalty in case of mines. Minimum Rent is also known as Fixed Rent, Dead Rent, Flat Rent or Contract Rent. If in any year amount of royalty is less than the amount of minimum rent, the amount of minimum rent is payable by the person who has to pay the royalty, but if the amount of royalty is more than the amount of minimum rent, royalty will be paid.

Importance of Minimum Rent:

Fixation of minimum rent is in the interest of landlord because it guarantees him the receipt of the minimum rent even in the case of low output or sales. In the absence of minimum rent clause, only the actual royalty will be paid to the landlord. Moreover, it also gives incentive to the lessee to enhance production or sales because he is bound to pay minimum rent.

(ii) What do you mean by ‘recoupment of Shortworkings’? What conditions are to be fulfilled for recoupment of Shortworkings? 2+3=5

Ans: Recoupment of Shortworkings: Recoupment of short working refers to recovering the short working of any year, from surplus royalty of the succeeding years. The right of recoupment of Shortworkings can be:

- Restricted or Fixed period or

- Unrestricted or Floating period.

When the lessee gets the right of recoupment of Shortworkings for a certain period (say first five years of the lease) commencing from the date of the royalty agreement, the right is said to be restricted or fixed. Any Shortworkings arising beyond this period cannot be reimbursed. But when the lessor allows the lessee to recoup any Shortworkings within two or three subsequent or following years, then the right is said to be unrestricted or floating because this can be availed of in any year when Shortworkings arises.

Conditions for Recoupment or Writing off Shortworkings:

Shortworkings can be recouped only when there is surplus. The Recoupment may be permitted over a stipulated period of time (fixed Recoupment) or over a specified period following the year of short working (floating Recoupment) or within the life time of the lease(Recoupment within life time of the lease). All the conditions regarding recoupment or writing off Shortworkings are based on the mutual agreement between the lessee and lessor. If Shortworkings could not be recouped within the agreed period, it will be transferred to profit and loss account in the year in which the right of recoupment is lost. By this process, Shortworkings account gets closed and will not appear as an asset in the balance sheet.

Or

(b) Raju took a lease of a mine on 01.01.2011 for a period of 20 years. Royalty payable is Rs. 1 per ton subject to a minimum rent of Rs. 12,000 per annum. The Shortworkings are recoupable during the first three years of the lease. The output was:

Year 2011

Year 2012

Year 2013

Year 2014

|

NIL

4000 tons

20000 tons

40000 tons

|

Give Journal Entries in the books of Raju to record the above transactions. 11

Solution:

7. (a) What do you mean by ‘amalgamation’? What are the different methods of amalgamation? Mention about the objectives and advantages of amalgamation. Out of syllabus 2+3+3+3=11

Or

(b) In a partnership firm, Arun and Barun are sharing profits and losses in the ratio of 5:3. They decided to dissolve their firm as on 31st March, 2015. Their Balance Sheet as on 31st March, 2015 is given below:

Balance Sheet

Liabilities

|

Rs.

|

Assets

|

Rs.

|

Creditors

Loan from Arun

Loan from Barun

Capital:

Arun 8,000

Barun 5,400

|

9,316

3,684

600

13,400

|

Goodwill

Furniture

Machinery

Inventory

Debtors

Cash

|

4,000

1,000

2,000

9,200

10,000

800

|

27,000

|

27,000

|

The assets realised as follows:

Goodwill

Furniture

Inventory

Debtors

Machinery

|

Rs.

2,600

900

8,300

10,200

8,800

|

Creditors were paid Rs. 9,120 in full settlement of their claim. Realisation expenses amounted to Rs. 110. A bill for Rs. 130 due for sales tax was received during the course of realisation and this was also paid. Close the books of the firm. 11