[Budget and Budgetary Control Notes, Management Accounting Notes, Notes For B.Com, BBA and MBA Students, Responsibility Account, Types of Budget]

Meaning and Definition of Budget, Budgeting and Budgetary Control:

Budget: A budget is the monetary and / or

quantitative expression of business plans and policies to be pursued in the

future period of time. Budgeting is preparing budgets and other procedures for

planning, coordination and control or business enterprises.

I.C.M.A.

defines a budget as “A financial and / or quantitative statement, prepared

prior to a defined period of time, of the policy to be pursued during that

period for the purpose of attaining a given objective”.

Budgeting refers to the process of preparing the

budgets. It involves a detailed study of business environment clearly grasping

the management objectives, the available resources of the enterprise and

capacity of the enterprise.

Budgeting

is defined by J.Batty as under: “The entire process of preparing the budgets is

known as budgeting”.

Thus

budgeting is a process of making the budget plans. Preparation of budgets or

budgeting is a planning function and their implementation is a control

function. ‘Budgetary control’ starts with budgeting and ends with control.

Budgetary control is the process of preparation of

budgets for various activities and comparing the budgeted figures for arriving

at deviations if any, which are to be eliminated in future. Thus budget is a

means and budgetary control is the end result. Budgetary control is a

continuous process which helps in planning and coordination. It also provides a

method of control.

According

to Brown and Howard “Budgetary control is a system of coordinating costs which

includes the preparation of budgets, coordinating the work of departments and

establishing responsibilities, comparing the actual performance with the

budgeted and acting upon results to achieve maximum profitability”.

Wheldon

characterizes budgetary control as planning in advance of the various functions

of a business so that the business as a whole is controlled.

I.C.M.A.

define budgetary control as “the establishment of budgets, relating the

responsibilities of executives to the requirements of a policy, and the

continuous comparison of actual with budgeted results either to secure by

individual actions the objectives of that policy or to provide a basis for its

revision”.

Characteristics / Features of Budgetary Control:

A budgetary control system can be defined as the establishment of budgets

relating to the responsibilities of executives to the requirements of a policy,

and the continuous comparison of actual with budgeted results either to secure

by individual action the objective of that policy or to provide a base for its

revision.

The salient features of such a system are the following:

(a) Objectives:

Determining the objectives to be achieved, over the budget period, and the

policy or policies that might be adopted for the achievement of these ends.

(b) Activities:

Determining the variety of activities that should be undertaken for the

achievement of the objectives.

(c) Plans:

Drawing up a plan or a scheme of operation in respect of each class of activity

in physical as well as monetary terms for the full budget period and its part.

(d) Performance

evaluation: Laying out a system of comparison of actual performance by each

person, section or department with the relevant budget arid determination of

causes for the discrepancies, if any.

(e) Control

Action: Ensuring that corrective action will be taken where the plan is not

being achieved and, if that is not

possible, for the revision of the plan.

Management Accounting | |

Chapter Wise Notes | Chapter Wise MCQs |

1. Introduction to Management Accounting 5. Budget and Budgetary Control Also Read: | |

Management Accounting Important Questions for Upcoming Exams (Dibrugarh University) | |

Management Accounting Solved Papers: 2013 2014 2015 2016 2017 2018 2019 | |

Management Accounting Question Papers: 2013 2014 2015 2016 2017 2018 2019 | |

Objectives and Importance of Budgetary Control System:

Budgets are very important for management. The need and objectives of a budgetary control system are listed below:

a)

Planning: A budget provides a

detailed plan of action for a business over definite period of time. Detailed

plans relating to production, sales, raw material requirements, labour needs,

advertising and sales promotion performance, research and development

activities, capital additions etc., are drawn up. By planning many problems are

anticipated long before they arise and solutions can be sought through careful

study. Thus most business emergencies can be avoided by planning. In brief,

budgeting forces the management to think ahead, to anticipate and prepare for the

anticipated conditions.

b)

Co-ordination: Budgeting aids

managers in co-coordinating their efforts so that objectives of the

organisation as a whole harmonise with the objectives of its divisions.

Effective planning and organisation contributes a lot in achieving

coordination. There should be coordination in the budgets of various

departments. For example, the budget of sales should be in coordination with

the budget of production. Similarly, production budget should be prepared in

co-ordination with the purchase budget, and so on.

c)

Communication: A budget is a

communication device. The approved budget copies are distributed to all

management personnel who provide not only adequate understanding and knowledge

of the programmes and policies to be followed but also gives knowledge about

the restrictions to be adhered to. It is not the budget itself that facilitates

communication, but the vital information is communicated in the act of

preparing budgets and participation of all responsible individuals in this act.

d)

Motivation: A budget is a useful

device for motivating managers to perform in line with the company objectives.

If individuals have actively participated in the preparation of budgets, it act

as a strong motivating force to achieve the targets.

e)

Control: Control is necessary to

ensure that plans and objectives as laid down in the budgets are being

achieved. Control, as applied to budgeting, is a systematized effort to keep

the management informed of whether planned performance is being achieved or

not. For this purpose, a comparison is made between plans and actual

performance. The difference between the two is reported to the management for

taking corrective action.

f)

Performance Evaluation: A budget

provides a useful means of informing managers how well they are performing in

meeting targets they have previously helped to set. In many companies, there is

a practice of rewarding employees on the basis of their achieving the budget

targets or promotion of a manager may be linked to his budget achievement record.

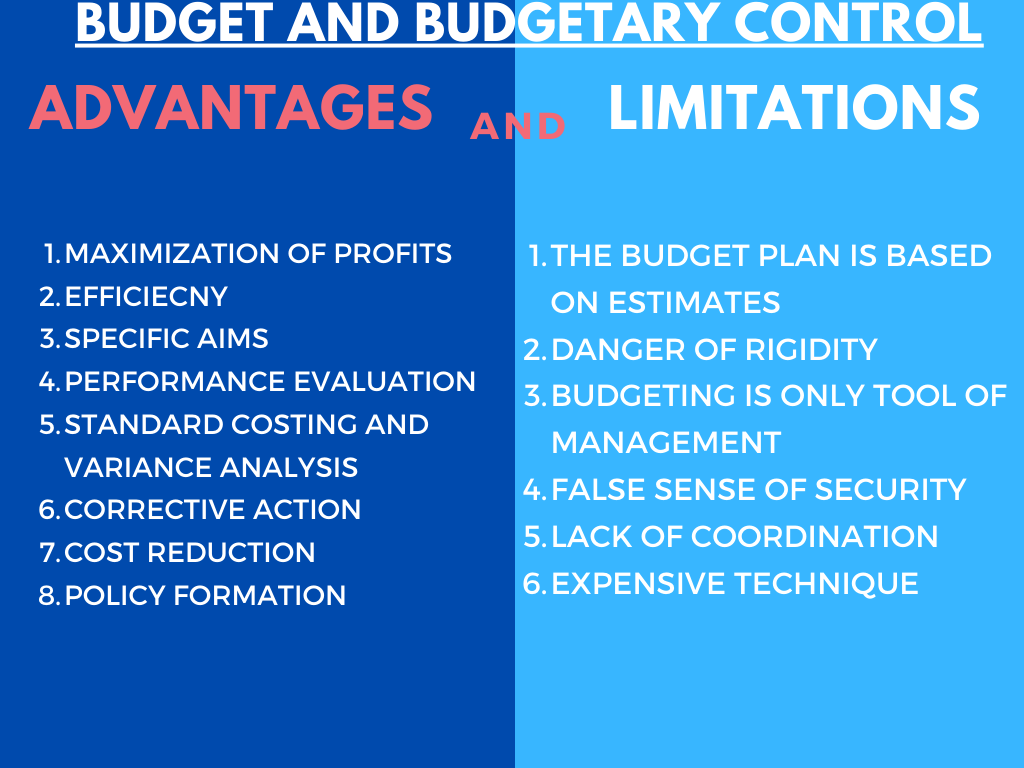

Advantages and Limitations of Budgetary Control:

Advantages of Budgetary Control System:

A budget is a blue print of a plan expressed

in quantitative terms. Budgeting is technique for formulating budgets. Budgetary Control, on the

other hand, refers to the principles,

procedures and practices of achieving given objectives through budgets. Here are

the some Advantages of Budgetary Control:

a)

Maximization

of Profit: The budgetary control aims at the maximization of profits of the enterprise. To achieve this aim, a proper planning and

co-ordination of different functions is undertaken. There is proper control

over various capital and revenue expenditures. The resources are put to the

best possible use.

b)

Efficiency: It enables the

management to conduct its business activities in an efficient manner. Effective

utilization of scarce resources, i.e. men, material, machinery, methods and

money - is made possible.

c)

Specific

Aims: The plans, policies and goals are decided by the top management.

All efforts are put together to reach the common goal of the organization.

Every department is given a target to be achieved. The efforts are directed towards achieving come specific aims. If there is no

definite aim then the efforts will be wasted in pursuing different aims.

d)

Performance evaluation: It provides

a yardstick for measuring and evaluating the performance of individuals and

their departments.

e)

Economy: The planning of expenditure will be systematic and there will be

economy in spending. The finances will be put to optimum use. The benefits

derived for the concern will ultimately extend to industry and then to national

economy. The national resources will be used economically and wastage will be

eliminated.

f)

Standard Costing and Variance analysis:

It creates suitable conditions for the implementation of standard costing system

in a business organization. It reveals the deviations to management from the

budgeted figures after making a comparison with actual figures.

g)

Corrective

Action: The management will be able to take corrective measures whenever

there is a discrepancy in performance. The deviations will be regularly

reported so that necessary action is taken at the earliest. In the absence of a

budgetary control system the deviation can determined only at the end of the

financial period.

h)

Consciousness: It creates budget consciousness among the employees. By fixing

targets for the employees, they are made conscious of their responsibility.

Everybody knows what he is expected to do and he continues with his work

uninterrupted.

i)

Reduces

Costs: In the present day competitive world budgetary control has a

significant role to play. Every businessman tries to reduce the cost of

production for increasing sales. He tries to have those combinations of

products where profitability is more.

j)

Policy formulation: It helps in the

review of current trends and framing of future policies.

Problems and Limitations of Budgetary Control System:

The list of advantages given above is impressive, but a budget is not a

cure all for organisational ills. Budgetary control system suffers from certain

limitations and those using the system should be fully aware of them.

a)

The budget plan is based on estimates:

Budgets are based on forecasting cannot be an exact science. Absolute accuracy,

therefore, is not possible in forecasting and budgeting. The strength or

weakness of the budgetary control system depends to a large extent, on the

accuracy with which estimates are made. Thus, while using the system, the fact

that budget is based on estimates must be kept in view.

b)

Danger of rigidity: Budgets are

considered as rigid document. Too much emphasis on budgets may affect

day-to-day operations and ignores the dynamic state of organization

functioning.

c)

Budgeting is only a tool of management:

Budgeting cannot take the place of management but is only a tool of management.

‘The budget should be regarded not as a master, but as a servant.’ Sometimes it

is believed that introduction of a budget programme alone is sufficient to

ensure its success. Execution of a budget will not occur automatically. It is

necessary that the entire organisation must participate enthusiastically in the

programme for the realisation of the budgetary goals.

d)

False Sense of Security: Mere

budgeting cannot lead to profitability. Budgets cannot be executed

automatically. It may create a false sense of security that everything has been

taken care of in the budgets.

e)

Lack of coordination: Staff

co-operation is usually not available during budgetary control exercise.

f)

Expensive Technique: The

installation and operation of a budgetary control system is a costly affair as

it requires the employment of specialized staff and involves other expenditure

which small concerns may find difficult to incur. However, it is essential that

the cost of introducing and operating a budgetary control system should not

exceed the benefits derived there from.

Essentials of Effective Budgeting:

A budgetary control system can prove successful only when certain

conditions and attitudes exist, absence of which will negate to a large extent

the value of a budget system in any business. Such conditions and attitudes

which are essential for an effective budgetary control system are as follows:

a)

Support of Top Management: If the

budget system is to be successful, it must be fully supported by every member

of the management and the impetus and direction must come from the very top

management. No control system can be effective unless the organisation is

convinced that the top management considers the system to be import.

b)

Participation by Responsible Executives:

Those entrusted with the performance of the budgets should participate in the

process of setting the budget figures. This will ensure proper implementation

of budget programmes.

c)

Reasonable Goals: The budget figures

should be realistic and represent reasonably attainable goals. The responsible

executives should agree that the budget goals are reasonable and attainable.

d)

Clearly Defined Organisation: In

order to derive maximum benefits from the budget system, well defined

responsibility centers should be built up within the organisation. The

controllable costs for each responsibility centres should be separately shown.

e)

Continuous Budget Education: The

best way to ensure the active interest of the responsible supervisors is

continuous budget education in respect of objectives, potentials &

techniques of budgeting. This may be accomplished through written manuals,

meetings etc., whereby preparation of budgets, actual results achieved etc.,

may be discussed.

f)

Adequate Accounting System: There is

close relationship between budgeting and accounting. For the preparation of

budgets, one has to depend on the accounting department for reliable historical

data which primarily forms the basis for many estimates. The accounting system

should be so designed so as to set up accounts in terms of areas of managerial

responsibility. In other words, responsibility accounting is essential for

successful budgetary control.

g)

Constant Vigilance: Reports

comparing budget and actual results should be promptly prepared and special

attention focused on significant exceptions i.e. figures that are significantly

different from those expected.

h)

Maximum Profit: The ultimate object

of realizing the maximum profit should always be kept uppermost.

i)

Cost of the System: The budget

system should not cost more than it is worth. Since it is not practicable to

calculate exactly what a budget system is worth, it only implies a caution

against adding expensive refinements unless their value clearly justifies them.

j)

Integration with Standard Costing System:

Where standard costing system is also used, it should be completely integrated

with the budget programme, in respect of both budget preparation and variance

analysis.

Essentials Factors and Elements for the Success of Budgetary Control

There

are certain steps which are necessary for the successful implementation of a

budgetary control system. They are as follows:

1.

Organization

for Budgetary Control: The proper organization is essential for the

successful preparation, maintenance and administration of budgets. A budgetary

committee is formed which comprises the departmental heads of various

departments. All the functional heads of various departments are entrusted with

the responsibility of ensuring proper implementation of their respective

departmental budgets. This has been shown in the following chart.

2.

Budget

Centres: A budget centre is that part of the organization for which the

budget is prepared. A budget centre may be a department, section of a

department or any other part of the department. The establishment of budget

centres is essential for covering all parts of the organization. The budget

centres are also necessary for cost control purposes. The appraisal of

performance of different parts of the organization becomes easy when different

centres are established.

3.

Budget

Manual: A budget manual is a document which tells out the duties and also

responsibilities of various executives concerns with the budgets. It specifies

the relation among various functionaries. A budget manual covers the following:

1)

A budget manual clearly defines the objectives

of budgetary control system. It also gives the benefits and principles of this

system.

2)

The duties and responsibilities of various

persons dealing with preparation and execution of budgets are also given in a

budget manual. It enables the management to know of persons dealing with

various aspects of budgets and clarify their duties and responsibilities.

3)

It gives information about the sanctioning authorities

of various budgets. The financial powers of different managers are given in the

manual for enabling the spending of amount on various expenses.

4)

A proper table for budgets including the

sending of performance reports is drawn so that every work starts in time and a

systematic control is exercised.

5)

The specimen forms and number of copies to be

used for preparing budget reports will also be stated. Budget centres involved

should be clearly stated.

6)

The length of various budget periods and

control points be clearly given.

7)

The procedure to be followed in the entire

system should be clearly stated.

8)

A method of accounting to be used for various

expenditures should also be stated in the manual.

4.

Budget

Officers: The chief executive who is at the top of the organization appoints

some person as budget officer. The budget officer is empowered to scrutinize

the budgets prepared by different functional heads and to make changes in them,

if the situation so demands. The actual performance of department is

communicated to the budget officer. He determines the deviation in the budgets

and takes necessary steps to rectify the deficiencies.

5.

Budget

Committee: In small scale concerns, the accountant is made responsible for

preparation and implementation of budgets. In large scale concerns a committee

known as budget committee is formed. The heads of all departments are made

members of this committee. The committee is responsible for preparation and

execution of budgets. The members of this committee put up the case of their

respective departments and help the committee to take collective discussions.

The budget office acts as coordinator of this committee.

6.

Budget

Period: A budget period is the length of time for which a budget is

prepared. The budget period depends upon a number of factors. It may be

different for different industries or even it may be different in the same

industry or business.

7.

Determination

of Key Factors: The budgets are prepared for all functional areas. These budgets

are inter-departmental and inter-related. A proper coordination amount

different budget is necessary for making the budgetary control a success. The

constraints on some budgets may have an effect on other budgets too. A factor

which influences all other budgets is known as Key Factor or Principal Factor.

There may be a limitation on the quality of goods a concern may sell. In this

case, sales will be a key factor and all other budgets will be prepared by

keeping in view the amount of goods the concern will be able to sell. The raw

material supply may be limited; so production, sales and cash budgets will be

decided according to raw materials budget. Similarly, plant capacity may be key

factor if the supply of other factor is easily available.

Zero Based Budgeting

ZBB is defined as ‘a method of budgeting which requires each cost element

to be specifically justified, as though the activities to which the budget

relates were being undertaken for the first time. Without approval, the budget

allowance is zero’.

Zero – base budgeting is so called because it requires each budget to be

prepared and justified from zero, instead of simple using last year’s budget as

a base. In Zero Based budgeting no reference is made to previous level

expenditure. Zero based budgeting is completely indifferent to whether total

budget is increasing or decreasing.

‘Zero base budgeting’ was originally developed by Peter A. Pyher at Texas

Instruments. Peter A. Pyher has defined ZBB as “an operating, planning and

budgeting process which requires each manager to justify his entire budget

request in detail from scratch (hence zero base) and shifts the burden of proof

to each manager to justify why we should spend any money at all”.

CIMA has defined it “as a method of budgeting whereby all activities are

revaluated each time a budget is set."

Zero Base Budgeting Advantages and Disadvantages

Zero Base Budgeting has the folowing advantages:

a) Zero base budgeting examines all existing and new programmes and activities.

It also makes the managers analyse

their functions, establish priorities and rank them. This exercise helps in identifying inefficient or obsolete

functions within the area of responsibility. In this

way resources are allocated from low priority programmes to high priority programmes.

b)

This system facilitates

identification of duplication of efforts among organisational units. Such inefficient activities are eliminated and some other

activities are merged.

c)

All expenditures, under this

system are critically reviewed and justified and all operations activities are evaluated in greater detail in terms of

their cost- effectiveness and

cost-benefits. This requires managers to find alternative ways of performing their activities which may result in more efficient

procedures.

d)

ZBB promotes the tendency to

initiate studies and improvements during the period of operation as the persons

at the helm of affairs know that the process would be exercised next year and their knowledge and training

would enhance efficiency and

cost-effectiveness.

e)

ZBB provides for quick budget

adjustments during the year. If revenue falls short in this process, it offers the capability to quickly and

rationally modify goals and expectations to correspond to a

realistic and affordable plan of operations.

f)

ZBB ensures greater

participation of personnel in formulation and ranking processes. This helps in promoting level of job satisfaction and

thus resulting in better control and operational

efficiency in the organisation.

g)

Zero base budgeting is a

flexible tool that can be applied on a selective basis. It does not have to be applied throughout the entire organisation or

even in all the service departments. Keeping in

view the limitations of time, money and persons available to install, operate and monitor it the management thus

can select priority areas to which zero base

budgeting may be applied.

Zero Base Budgeting has the following disadvantages / Limitations:

a)

It challenges the past

practices, performance, attitudes, of people.

b)

It requires more time and

effort.

c)

Detailed costs and necessary

information for decision packages often are not made available.

d)

It increases paper work to

unmanageable proportions.

e)

Ranking a large number of

decision packages becomes an unwieldy process.

f) Identifying various levels of funding, particularly the minimum

level is a difficult task.

Steps in Zero-Base Budgeting

a)

Determination

of Objectives: The first step in ZBB is the clear definition of the

objectives of budgeting. The objective may be to reduce expenditure on staff,

to discontinue an activity or project in preference to another etc.

b)

Determination

of the Extent of Application: Whether ZBB should be introduced in all

operational areas or only in some selected areas is to be decided.

c)

Identification

of Decision Units: Decision unit refers to a department, a project or a

product line to which ZBB is to be applied. Identification of such units is

done in consultation with managers.

d)

Cost-Benefit

Analysis: Cost benefit analysis is undertaken for each activity of the

decision unit. It provides answers to the following questions.

1.

Is it necessary to perform the activity at all?

If the answer is in the negative, there is no need for proceeding further.

2.

How much is the actual cost and what is the

actual benefit of the activity?

3.

What is the estimated cost and estimated benefit

of the activity?

4.

If the unit is dropped, can the unit be replaced

by outside agency?

e)

Preparation

of budgets: The activities and projects for which benefit is more than the

cost are ranked. Priority is accorded to the most

profitable projects/activities, in the allocation of funds.

Cash Budget

A cash budget is a budget or plan of expected cash receipts and

disbursements during the period. These cash inflows and outflows include

revenues collected, expenses paid, and loans receipts and payments. In other

words, a cash budget is an estimated projection of the company's cash position

in the future.

Management usually develops the cash budget after the sales, purchases,

and capital expenditures budgets are already made. These budgets need to be

made before the cash budget in order to accurately estimate how cash will be

affected during the period. For example, management needs to know a sales

estimate before it can predict how much cash will be collected during the

period. Management uses the cash budget to manage the cash flows of a company.

In other words, management must make sure the company has enough cash to pay

its bills when they come due.

Chartered

Institute of Management Accountant (CIMA) defines cash budgets as a short-term

fiscal plan expressed in money which is prepared in advance. It helps to

determine the cash-inflow and cash-outflow of the business.

Features of Cash Budget

a)

The

cash-budget period is broken down into periods, mainly in months.

b)

The cash-budget

is always in columnar form i.e. column showing each month

c)

Payments

and receipts of cash are identified in different heading and showing total for

each month.

d)

The

surplus of total cash payment over receipts or of receipts over payment for

each month is shown.

e)

The

running balances of cash, which would be determined by taken the balance at the

end of the previous month and adjusting it for either deficit or surplus of

receipts over payments for current month, is identified.

Importance / Uses of Cash Budget

Cash budget is an important tool in the

hands of financial management for the planning and control of the working

capital to ensure the solvency of the firm. The importance of cash budget may be summarised as

follow:

(1) Helpful in Planning. Cash

budget helps planning for the most efficient use of cash. It points out cash

surplus or deficiency at selected point of time and enables the management to

arrange for the deficiency before time or to plan for investing the surplus

money as profitable as possible without any threat to the liquidity.

(2) Forecasting the Future needs. Cash

budget forecasts the future needs of funds, its time and the amount well in

advance. It, thus, helps planning for raising the funds through the most

profitable sources at reasonable terms and costs.

(3) Maintenance of Ample cash Balance. Cash is

the basis of liquidity of the enterprise. Cash budget helps in maintaining the

liquidity. It suggests adequate cash balance for expected requirements and a

fair margin for the contingencies.

(4) Controlling Cash Expenditure. Cash

budget acts as a controlling device. The expenses of various departments in the

firm can best be controlled so as not to exceed the budgeted limit.

(5) Evaluation of Performance. Cash

budget acts as a standard for evaluating the financial performance.

(6) Testing the Influence of proposed

Expansion Programme. Cash budget forecasts the inflows from a proposed

expansion or investment programme and testify its impact on cash position.

(7) Sound Dividend Policy. Cash

budget plans for cash dividend to shareholders, consistent with the liquid

position of the firm. It helps in following a sound consistent dividend policy.

(8) Basis of Long-term Planning and

Co-ordination. Cash budget helps in co-coordinating the various

finance functions, such as sales, credit, investment, working capital etc. it

is an important basis of long term financial planning and helpful in the study

of long term financing with respect to probable amount, timing, forms of

security and methods of repayment.

Methods of Preparation of Cash Budget

(1) Receipts and Payments Method

(2) Adjusted Profit and Loss Method or Adjusted Earnings

Method or Cash Flow Method.

(3) Balance-Sheet Method.

The above methods of preparing cash budget represent different

approaches.

(1) Receipts and Payments Method: It

is the most simple and popular method of preparing cash budget. The method is

most commonly used in forecasting the short term cash position. It is just

like receipts and payment method in technique. It shows yearly cash position

with proper breakups by quarters and months. For the purpose of preparing cash

budget under this method, cash information’s are collected from other budgets

such as sales budget, salary and wages budget, overhead budgets, material

budget etc.

Under this method cash budget is divided into two parts. One part shows

the timing and the amount of cash receipts and other part shows the timing and

the amount of cash disbursements. Cash receipts and cash disbursements are

estimated as under:

(i)

Estimation of Cash Receipts: The

amount of cash receipts can be estimated from the following items:

(a)

Cash receipts arising from

Operations. It includes advances form customers, estimated cash

receipts from sales, debtors and collection of bills receivables. In estimating

the amount of cash sales, cash-discount policy of the firm should be taken into

account. Forecasting the receipts from credit sales, i.e., receipts from

customers, B/R etc. Credit policy, terms of sales, position of customers, customers

of the trade, any time lag between sale and collection should be considered.

(b)

Non-operating Cash Receipts. It

includes revenue receipts of non-operating nature and includes receipts from

interest, dividend, rent, commission, royalty, sale of scrap, refund of tax

etc.

(ii) Estimation of Cash Disbursements. The amount

of cash disbursement can be estimated from the following items:

(a) Disbursement for operations Such as

disbursements for cash purchases, wages and overheads, payment to creditors,

bonus and other remunerations such as gratuities, pensions etc. and advances to

suppliers. Terms of purchases, discounts receivable and time lag between the

time of purchase and payment are taken into consideration.

(b) Disbursement for non-operating functions. It

includes financial expenses on non operative functions such as interest, rent,

dividend, donations, income tax and other taxes etc.

(c) Disbursement for capital transactions. Such

as expenditure for expansion, payment of loans and overdrafts, redemption of

debentures and preference capital etc.

In preparing cash budget, total budgeted cash receipts are

added to the opening balance of cash and then the total budgeted disbursements

are deducted there from to know the closing balance of cash. If opening cash

balance and estimated total cash receipts are much larger than the estimated

payments, there will be cash balance at close and management should take the

necessary steps, to invest surplus funds for short period. On the other hand,

if there is cash shortage, the management must plan the borrowings for short

period to manage the deficiency.

(2) Adjusted

Profit and Loss Method or Adjusted Earnings Method or Cash Flow Method: The

method is suitable for preparing the long term estimates of cash inflows and

outflows. It is also called cash-flow statement. Under this method, profit and

loss account is adjusted to know the cash estimates. This method is useful in

budgetary control technique.

Under this method, closing cash balance can be known by

adding profits for the period to the opening cash balance because the theory is

based on the elementary assumption that profits of a business are equal to

cash. Thus if we assume that there are no credit transactions, capital

transactions, accruals, provisions, stock fluctuations, or appropriations of

profit, the balance of profit as shown by the profit and loss account should b

equal to the cash balance in the case book. However, such a situation will

never exist in actual practice, the assumption needs adjustments. In preparing

the cash forecasts, one proceeds with the budgeted profit for the period and

then adjusts this figure by the items mentioned below-

Items to be Added

(i) All non-cash items shown in the debit side of

profit and loss account should be added to the budgeted profit because these

items do not involve any cash outflows-depreciation, deferred revenue

expenditure, writing off of intangible assets, prepaid expenses etc.

(ii) Changes in working capital which results in

inflow of cash balances such as increase in closing stock, debtors and decrease

in sundry creditors and other liabilities, redemption of preference shares and

debentures, payment of dividend, purchase capital assets, investment etc.

(3) Balance-Sheet

Method: This method is similar to that of profit and loss adjustment

method, a budgeted balance sheet is prepared for the next period showing all

items of assets and liabilities except cash balance which is found out as the

balancing figure of the two sides of balance sheet.

If the asst side exceeds the liability side the balance shall

reveal the bank over-draft and if the liability side is heavier than the asset

side, the difference represents the bank balance.

Types of Budgets

As budgets serve

different purposes, different types of budgets have been developed. The

following are the different classification of budgets developed on the basis of

time, functions, and flexibility or capacity.

(A) Classification on the basis of Time:

1. Long-term

budgets

2. Short-term

budgets

3. Current

budgets

(B) Classification according to functions:

1. Functional or

subsidiary budgets

2. Master budgets

(C) Classification on the basis of capacity:

1. Fixed budgets.

2. Flexible

budgets

(A)

Classification on the basis of time

1. Long-term budgets: Long-term budgets are prepared for a longer period varies between

five to ten years. It is usually developed by the top level management. These

budgets summarise the general plan of operations and its expected consequences.

Long-term budgets are prepared for important activities like composition of its

capital expenditure, new product development and research, long-term finance

etc.

2. Short-term budgets: These budgets are usually prepared for a

period of one year. Sometimes they may be prepared for shorter period as for quarterly

or half yearly. The scope of budgeting activity may vary considerably among

different organization.

3. Current budgets: Current budgets are prepared for the current operations of the

business. The planning period of a budget generally in months or weeks. As per

ICMA London, “Current budget is a budget which is established for use over a

short period of time and related to current conditions.”

(b)

Classification on the basis of function

1. Functional budget: The functional budget is one which relates to any of the functions

of an organization. The number of functional budgets depends upon the size and

nature of business. The following are the commonly used:

(i) Sales budget

(ii) Purchase

budget

(iii) Production

budget

(iv) Selling and

distribution cost budget

(v) Labour cost

budget

(vi) Cash budget

(vii) Capital

expenditure budget

2. Master budget: The master budget is a summary budget. This budget encompasses all

the functional activities into one harmonious unit. The ICMA England defines a

Master Budget as the summary budget incorporating its functional budgets, which

is finally approved, adopted and employed.

(C)

Classification on the basis of capacity

1. Fixed budget: A fixed budget, on the other hand is a budget

which is designed to remain unchanged irrespective of the level of activity

actually attained. In a fixed budgetary control, budgets are prepared for one

level of activity whereas in a flexibility budgetary control system, a series

of budgets are prepared one for each level of alternative production levels or

volumes. According

to ICWA London ‘Fixed budget is a budget which is designed to remain unchanged

irrespective of the level of activity actually attained.”

Fixed budget is

usually prepared before the beginning of the financial year. This type of

budget is not going to highlight the cost variance due to the difference in the

levels of activity. Fixed budgets are suitable under static conditions.

2. Flexible budget: Flexible Budget: A flexible budget is defined

as “a budget which, by recognizing the difference between fixed, semi-variable

and variable cost is designed to change in relation to the level of activity

attained”. Flexible budgets represent the amount of expense that is reasonably

necessary to achieve each level of output specified. In other words, the

allowances given under flexibility budgetary control system serve as standards

of what costs should be at each level of output.

According to

ICMA, England defined Flexible Budget is a budget which is designed to change

in accordance with the level of activity actually attained.”

According to the

principles that guide the preparation of the flexible budget a series of fixed

budgets are drawn for different levels of activity. A flexible budget often

shows the budgeted expenses against each item of cost corresponding to the

different levels of activity. This budget has come into use for solving the

problems caused by the application of the fixed budget.

Advantages

of flexible budget

1. In flexible

budget, all possible volume of output or level of activity can be covered.

2. Overhead costs

are analysed into fixed variable and semi-variable costs.

3. Expenditure

can be forecasted at different levels of activity.

4. It facilitates

at all times related factor can be compared, which essential for intelligent

decision are making.

5. A flexible

budget can be prepared with standard costing or without standard costing

depending upon what the company opts for.

6. A flexible

budget facilitates ascertainment of costs at different levels of activity,

price fixation, placing tenders and quotations.

7. It helps in

assessing the performance of all departmental heads as the same can be judged

by terms of the level of activity attained by the business.

Method

of preparing flexible budget

The following methods

are used in preparing a flexible budget:

1. Multi-activity

method

2. Ratio method

3. Charting

method.

1. Multi-Activity method: This method involves preparing a budget in

response to different level of activity. The different level of activity or capacity

levels are shown in Horizontal columns, and the budgeted figures against such

levels are placed in the Vertical Columns. The expenses involved in production

as per budget are grouped as fixed, variable and semi variable.

2. Ratio method: According to this method, the budget is prepared first showing the

expected normal level of activity and the estimated variable cost per unit at

the side expected level of activity in addition to the fixed cost as estimated.

Therefore, the expenses as per budget, allowed for a particular level of

activity attained, will be calculated on the basis of the following formula:

Budgeted fixed cost + (Variable cost per unit of activity × Actual unit of

activity).

3. Charting method: Under this method total expenses required for any level of

activity, are estimated having classified into three categories, viz.,

variable, semi variable and fixed. These figures are plotted on a graph. The

expenses are plotted on the Y-axis and the level of activity is plotted on

X-axis. The graphs will thus, help in ascertaining the quantum of budgeted

expenses corresponding to the level of activity attained with the help of this

chart.

Difference between Fixed Budget and Flexible Budget

|

|

Fixed Budget

|

Flexible Budget

|

|

1.

|

It does

not change with actual volume of activity achieved. Thus it is known as rigid

or inflexible budget.

|

It can

be recasted on the basis of activity level to be achieved. Thus it is not

rigid.

|

|

2.

|

It

operates on one level of activity and under one set of conditions. It assumes

that there will be no change in the prevailing conditions, which is

unrealistic.

|

It

consists of various budgets for different levels of activity.

|

|

3.

|

Here as

all costs like - fixed, variable and semi-variable are related to only one

level of activity. So variance analysis does not give useful information.

|

Here

analysis of variance provides useful information as each cost is analysed

according to its behaviour.

|

|

4.

|

If the

budgeted and actual activity levels differ significantly, then the aspects

like cost ascertainment and price fixation do not give a correct picture.

|

Flexible

budgeting at different levels of activity facilitates the ascertainment of

cost, fixation of selling price and tendering of quotations.

|

|

5.

|

Comparison

of actual performance with budgeted targets will be meaningless specially

when there is a difference between the two activity levels.

|

It

provides a meaningful basis of comparison of the actual performance with the

budgeted targets.

|

Sales Budget

Sales budget is

one of the important functional budgets. Sales estimate is the commencement of

budgeting may be both made in quantitative or in value terms. Sales budget is

primarily concerned with forecasting of what products will be sold in what

quantities and at what prices during the budget period. Sales budget is

prepared by the sales executives taking into account number of relevant and

influencing factors such as: Analysis of past sales, key factors, market

conditions, production capacity, government restrictions, competitor’s strength

and weakness, advertisement, publicity and sales promotion, pricing policy,

consumer behaviour, nature of business, types of product, company objectives,

salesmen’s report, marketing research’s reports, and product life cycle.

Production Budget

Production budget

is usually prepared on the basis of sales budget. But it also takes into

account the stock levels desired to be maintained. The estimated output of

business firm during a budget period will be forecast in production budget. The

production budget determines the level of activity of the produce business and

facilities planning of production so as to maximum efficiency. The production

budget is prepared by the chief executives of the production department. While

preparing the production budget, the factors like estimated sales, availability

of raw materials, plant capacity, availability of labour, budgeted stock

requirements etc. are carefully considered.

Difference

between Sales Budget and Production Budget

a) A sales Budget

is a schedule, which shows expected sales in both units and sales rupees for

the coming period. Whereas a production budget determines only the quantity to

be produced in coming period.

b) A sales Budget

is not prepared on the basis of production budget. But a production budget is

prepared on the basis of sales budget.

c) Stock levels

are not shown in sales budget. But, a production budget takes into account the

stock levels desired to be maintained.

d) Sales budget

is prepared by the sales executives. Whereas, production budget is prepared by

the chief executives of the production department.

e) Estimated

selling price is shown in sales budget. Whereas, production budget helps in

calculating production cost for estimated level of production.

Cost of production Budget

After preparation

of production budget, this budget is prepared. Production cost budgets show the

cost of the production determined in the production budget. Cost of production

budget is grouped in to material cost budget, labour cost budget and overhead

cost budget. Because it break up the cost of each product into three main

elements material, labour and overheads. Overheads may be further subdivided in

to fixed, variable and semi-fixed overheads. Therefore separate budgets

required for each item.

Master Budget

When the functional

budgets have been completed, the budget committee will prepare a master budget

for the target of the concern. Accordingly a budget which is prepared

incorporating the summaries of all functional budgets. It comprises of budgeted

profit and loss account, budgeted balance sheet, budgeted production, sales and

costs. The ICMA England defines a Master Budget as ‘the summary budget

incorporating its functional budgets, which is finally approved, adopted and

employed’. The master budget represents the activities of a business during a

profit plan. This budget is also helpful in coordinating activities of various

functional departments.

Control Ratios

Ratios are used

by the management to determine whether performance of its activities is going

on as per estimates or not. If the ratio is 100% or more, the performance is

considered as unsatisfactory. The following are the ratios generally calculated

for performance evaluation.

1. Capacity ratio: This ratio indicates the extent to which budgeted hours of activity

is actually utilised.

Capacity Ratio =

(Actual hours worked production/Budget hours) × 100

2. Activity ratio: This ratio is used to measure the level of activity attained

during the budget period.

Activity ratio =

(Standard hours for actual production/Budgeted hours) × 100

3. Efficiency ratio: This ratio shows the level of efficiency attained during the

budget period

Efficiency ratio

= (Standard hours for actual production/Actual hours worked) × 100

4. Calendar ratio: This ratio is used to measure the proportion of actual working

days to budgeted working days in a budget period.

Calendar ratio =

(Number of actual working days in a period/ Budgeted working days for the

period) × 100

Differences between Budgetary Control and Standard Costing

Both standard costing and budgetary control achieve the same objective of

maximum efficiency and cost reduction by establishing predetermined standards,

comparing actual performance with the predetermined standards and taking

corrective measures, where necessary. Thus, although both are useful tools to

the management in controlling costs, they differ in the following respects:

|

Budgetary Control

|

Standard Costing

|

|

Budgetary

control deals with the operations of a department of business as a whole.

|

Standard

costing is applied to manufacturing of a product, process or processes or

providing a service.

|

|

It is

extensive in its application, as it deals with the operation of department or

business as a Whole.

|

It is

intensive, as it is applied to manufacturing of a product or providing a

service.

|

|

Budgets are

prepared for sales, production, cash etc.

|

It is

determined by classifying recording and allocating expenses to cost unit.

|

|

It is a

part of financial account, a projection of all financial accounts.

|

It is a

part of cost account, a projection of all cost accounts.

|

|

Control is

exercised by taking into account budgets and actual. Variances are not

revealed through accounts.

|

Variances

are revealed through difference accounts.

|

|

Budgeting

can be applied in parts.

|

It cannot

be applied in parts.

|

|

It is more

expensive and broad in nature, as it relates to production, sales, finance

etc.

|

It is not

expensive because it relates to only elements of cost.

|

|

Budgets can

be operated with standards.

|

This system

cannot be operated without budgets.

|

Concept and Meaning of Responsibility Accounting

Responsibility

accounting is a system used in management accounting for control of costs. It

is used along with other systems like budgetary control and standard costing.

The organization is divided into different centers called “responsibility

centers” and each centre is assigned to a responsible person.

According

to Eric. L. Kohler “ Responsibility Accounting is the classification,

management maintenance, review and appraisal of accounts serving the purpose of

providing information on the quality and standards of performance attained by

persons to whom authority has been assigned.”

Responsibility accounting, therefore, represents a method of measuring

the performances of various divisions of an organization. The test to identify

the division is that the operating performance is separately identifiable and

measurable in some way that is of practical significance to the management.

Responsibility accounting collects and reports planned and actual accounting information

about the inputs and outputs of responsibility centers.

Characteristics / Features of Responsibility Accounting

1. It is a

control system used by top management for monitoring and controlling operations of a business.

2. It is based on

clearly defined functions and responsibilities assigned to executives.

3. The

organization is divided into meaningful segments called responsibility centres.

4. Costs and

revenues of each centre and responsibility of them are fixed on the individuals.

5. There is

continuous reporting of information relating to each centre and appropriate corrective actions are taken

wherever necessary.

6. It is used

along with budgetary and standard costing system

Steps in Responsibility Accounting

1. Identifying

Responsibility centres: The organization

is divided into meaningful segments based on functions. Each centre is assigned to a specified person.

He is responsible for the costs and performance of

that centre.

2. Fixing targets

for Responsibility centres: Targets are fixed

for each centre in terms of inputs and outputs or costs and revenues. The functions and targets are

clearly communicated to the bottom level persons.

3. Measuring the

actual performance: The performance

of each centre is continuously monitored and evaluated. There is a system to communicate this

information to the top management regularly.

4. Evaluating

performance: The actual

performance is compared with targets and variances are analyzed.

5. Taking

corrective measures: Whenever there is

an adverse variance in terms of cost, revenue or resources,

managerial control is exercised by taking corrective actions. Responsibility accounting like budgeting or

standard costing, is a control device. The whole

exercise is done to check inefficiencies, wastages and losses, thereby improving the overall performance of

the organization.

Advantages of Responsibility accounting

1. It is used for

exercising effective control on operations by fixing responsibilities on specific persons in an organization.

2. It helps to

increase profitability of the organization.

3. It helps in

the effective delegation of authority.

4. The managers

and employees will be more vigilant since their performances are constantly evaluated.

5. It helps in

the implementation of budgetary control and standard accounting system.

6. A good

reporting system is inevitable to Responsibility Accounting which facilitates quick decision making by

management.

Disadvantages of Responsibility Accounting

1. It is

difficult to identify and classify the responsibility centres

2. There will always

be conflict of interests among the responsibility centres and that may not be at the interest of the

organization as a whole.

3. It may not be

actually needed especially in small and medium organizations where there is already a system of budgetary control

and standard costing.

4. The

co-ordination of responsibility centres may be difficult if there are too many centres.

5. Resistance of

managers and lack of co-operation from employees may happen.

6. It needs a

detailed communication and reporting system which is very costly.

Performance Budgeting

Management Accounting | |

Chapter Wise Notes | Chapter Wise MCQs |

1. Introduction to Management Accounting 5. Budget and Budgetary Control Also Read: | |

Management Accounting Important Questions for Upcoming Exams (Dibrugarh University) | |

Management Accounting Solved Papers: 2013 2014 2015 2016 2017 2018 2019 | |

Management Accounting Question Papers: 2013 2014 2015 2016 2017 2018 2019 | |

Performance Budgeting had its origin in U.S.A. after the Second World

War. It tries to rectify some of the traditional budget. In the traditional

budget amount are earmarked for the objects of expenditure such as salaries,

travel, office expenses, grant in aid etc. In such system of budgeting the

money concept was given more prominence i.e. estimating or projecting rupee

value for the various accounting heads or classification of revenue and cost.

Such system of budgeting was more popularly used in government departments and

many business enterprises. But is such system of budgeting control of

performance in terms of physical units or the related costs cannot be achieved.

Performance oriented budgets are established in such a manner that each

item of expenditure related to a specific responsibility center is closely

linked with the performance of that center. The basic issue involved in the

fixation of performance budgets is that of developing work programmes and

performance expectation by assigned responsibility, necessary for the

attainments of goals and objectives of the enterprise, it involves

establishment of well defined centers of responsibilities, establishment for

each responsibility center – a programme

of target performance in physical units, forecasting the amount of expenditure

required to meet the physical plan laid down and evaluation of performance.

The main features

of performance budgeting are as follows:

a.

It

helps the management to regulate its each and every activity according to

predetermined standards of performance, targets and objectives.

b.

It

is not only an estimate of future needs but goes beyond that and- includes

functions, programmes, activity schemes and time schedules to help effective

and economic allocation for the programmes.

c.

It

lays great stress on the management of organisational structural and overall

policy, personnel, financial, etc. from traditional to dynamic one.

d.

It

is not merely a projection of trends and targets but planning the business from

grass root level to top level on rational thinking and forecasting.

Difference between Performance Budgeting and Traditional Budgeting

|

Performance

budgeting

|

Traditional

Budgeting

|

|

1)

In it, the flow of decision is upward.

2)

It follows the function – programme – activity

classification.

3)

It makes a prospective approach with its focus

on future markets.

|

1)

In it, the flow of decision is downward.

2)

In it, the classification of expenses is by

objects.

3)

The approach is retrospective in such budgeting.

|

Advantages of Performance Budgeting

a)

It presents clearly the purposes and objectives

for which funds are required.

b)

It gives better appreciation of budgeting by

legislature.

c)

It improves budget formulation process.

d)

It enhances accountability of the executives.

Post a Comment

Kindly give your valuable feedback to improve this website.